When it comes to retirement or transitioning out of dermatology practice and into some other professional endeavor, practice management pundits and those who have been through the experience agree that: Those who fail to plan, plan to fail.

When it comes to retirement or transitioning out of dermatology practice and into some other professional endeavor, practice management pundits and those who have been through the experience agree that: Those who fail to plan, plan to fail.

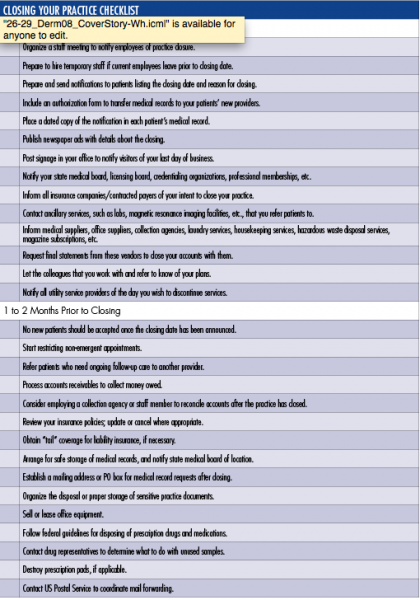

It’s never too soon to start planning for retirement because there are so many boxes on the to-do list that need to be checked before a dermatologist can transition into the next phase of his or her life without leaving loose ends dangling (See Checklist).

[Read Part 2 of this series, Three Key Steps in Retirement Planning: Part 2 here].

Former American Academy of Dermatology President Stephen Stone, MD, Southern Illinois University (SIU), School of Medicine, Springfield, IL, says it’s always a good idea to engage an accountant and attorney who are familiar with medical practice issues so they can guide you along in the process that includes everything from wrapping up the employee pension plan to obtaining a “tail” that provides coverage against claims reported after your regular liability insurance policy expires. Dr. Stone started out as a partner in a dermatology practice. After 2 associates moved on to teaching positions, Dr. Stone decided that, he, too, would make a similar switch.

“The main reason I left private practice was that I was in a solo situation, and I was burning out with respect to the practice management and the business aspects of the practice. I still loved seeing patients and I loved working with residents, but I knew I had to make a change,” he explains. While he was in private practice, he was a volunteer faculty member at SIU, and he says the best part of that was working with the residents. “So when I had the opportunity to close up my practice and take a teaching position, it was a perfect fit,” says Dr. Stone.

One of the most difficult parts of closing his practice was sharing the news with his employees. “Frankly, that played a part in delaying my decision because most of them were with me for quite a while. We were like a family. Some of them moved on to the medical school with me, and others I tried to help find jobs,” he says.

On a more practical note, Dr. Stone stresses, “You can’t just shut the practice and walk away. It’s a pretty complicated process. You have to bear in mind that your bills are not going to go out until after the very last day you see patients and money is going to trickle in for over a year. So, you’ve got to have arrangements for receiving, depositing and continuing to bill the outstanding receivables, among other things.”

Live and Learn

Former private practice dermatologist Haines Ely, MD, of Grass Valley, CA, is the perfect example of a dermatologist who lacked key knowledge necessary to effectively close up shop. “Something that is not common knowledge is that your expenses don’t stop just because you close the doors of the office. You continue to receive requests for medical records, insurance forms, overpayment/underpayment billings from Medicare, insurance companies and others. The paperwork continues for months,” he says. “I assumed that when I closed the doors, everything stopped — but it didn’t. So I learned that you need a staff — or someone — to take care of the continuing trail of papers.” He says he still gets requests from insurance companies about claims submitted 2 to 3 years ago.

Valuing Your Practice

Bellville, NJ-based dermatologist and dermatology practice management guru Joseph Eastern, MD, frequently writes about and makes presentation on the topic of retirement. The 2-time past-president of the Dermatological Society of New Jersey says when considering what steps to take if or when you decide to sell your practice the first hurdle is the accurate valuation of the practice. “It’s important that the appraisal be done by an experienced and neutral financial consultant, that all techniques used in the valuation be divulged and explained and that documentation is supplied to support the conclusions reached,” says Dr. Eastern.

It’s important to recognize that the valuation will not necessarily equal the purchase price, other factors may need to be considered before a final price can be agreed upon and there may be legal constraints on the purchase price. “For example,” says Dr. Eastern, “if the buyer is a non-profit corporation such as a hospital or health maintenance organization (HMO), by law it cannot pay in excess of fair market value for the practice.”

Once a value has been agreed upon, the seller must consider how the transaction will be structured. “The most popular structures include purchase of assets, purchase of corporate stock or merger,” says Dr. Eastern. “Buyers, especially institutional buyers, prefer to purchase assets, because it allows them to pick and choose only those items that have value to them,” he explains. Depending on the circumstances, an asset sale may still be to both parties’ advantage. “Sellers typically prefer to sell stock because it allows them to sell their entire practice, which is often worth more than the sum of its parts, and often provides tax advantages,” adds Dr. Eastern.

The third option — merger — continues to grow in popularity. Usually, this takes the form of a sale of the medical practice to a publicly-traded HMO, which issues its own stock in payment, explains Dr. Eastern. “Because such purchasers are exempt from the restrictions that apply to not-for-profit organizations, they can pay higher prices — and pay for goodwill — and the stock issued in payment offers the seller an opportunity to participate in future profits and appreciation of value.”

Stock ownership is not without risk, of course, so he stresses that tax issues must always be considered. “Most private practices are corporations, and the sale of corporate stock will result in a long-term capital gain which will be taxed (under current law) at 28%. It actually may benefit the seller to accept a slightly lower price if the sale can be structured to provide significantly lower tax treatment. However, any gain that does not qualify as a long-term capital gain will be taxed as regular income — currently around 40%, plus a social security tax of about 15%,” explains Dr. Eastern.

The seller may wish to continue working at the practice as an employee, and this is often to the buyer’s advantage as well, points out Dr. Eastern. “Transitioning to new ownership in stages often maximizes the value of the business by improving patient retention, and allows patients to become accustomed to the transition. However, care must be taken, with the aid of good legal advice, to structure such an arrangement in a way that minimizes concerns of fraud and abuse. Congress has created a “safe harbor” to allow continuing employment, but its scope is narrow and does not cover many common arrangements. To qualify, the sale of the practice, including any installment payments, must be completed within a year after an agreement is reached, and the seller cannot be in a position to make referrals to the buyer after a year.”

Just (Don’t) Do It

Las Vegas dermatologist Lucius Blanchard, MD, knows more about selling — and buying — dermatology practices than the average physician. His large group practice, Las Vegas Skin and Cancer Clinics acquired practices throughout Arizona and California a few years back when market conditions were better. “The problem with trying to sell a dermatology practice,” says Dr. Blanchard, “is that I can go somewhere and open a dermatology office for approximately $100,000 — depending on the area — and I can equip it, and put a physician in there, and in a year or two build up a very good practice. So why would I pay somebody $400,000 or $500,000 for a practice unless they are going to stay there for a few years to generate income and ensure that the patient base keeps growing. If they just want to sell and leave, there’s little value there.” Dr. Blanchard started off with 2 other dermatologists in 1 office and now has 25 offices throughout California, Arizona and Nevada.

Dr. Blanchard’s retirement advice to fellow dermatologists: Don’t do it. “As long as you’re healthy and can work, don’t retire. We have one of the best jobs anyone could have. It’s office-based, there’s very little emergency work and we don’t have as much risk as other specialists such as cardiovascular surgeons,” says Dr. Blanchard, “Plus, we can even selectively limit ourselves to low risk patients if we want to and limit our office hours so that we can structure our life pretty much how we want it to be.”

Despite Dr. Blanchard’s anti-retirement recommendation, clearly every dermatologist eventually reaches the point when passing the baton is appealing — or necessary. Some move on because they reach an age that they decided years before would be the appropriate time to make a change; others because their retirement account reaches a value that they decided years before would be adequate to support them through their twilight years and still others because they have had enough of managed care, government intervention, insurance company interference, complex electronic medical record technology and the mandate to document its meaningful use in order to avoid fines.

Dr. Ely says he would prefer to still be in private practice, but because of governmental interference he literally cannot afford to. It’s what prompted his retirement and his switch to academia. He is now a professor at University of California, Davis. “In 2011 my office manager informed me that by 2013, the graph of income versus expenses would cross in our practice and I would be working for nothing. By February of 2013, the lines crossed, and she came to me and said, ‘You are now officially working for nothing. Your expenses and your income are the same.’ I had no choice but to move on,” says Dr. Ely.

He explains, “I practiced in a small community with an independent practice association (IPA) that did the billing for all the physicians in the practice. Medicare audited the IPA and we were told that [Medicare] had to withhold a large amount of money for future claims, so the IPA had to withhold money from all of our claims, which diminished our income dramatically and the expenses kept going up.” He says he misses his private practice patients and the dynamic inherent in developing long-term connections with them. “I’m still seeing patients with residents, and that’s enjoyable, but it would have been nice to be able to stay in private practice,” he says.

While Dr. Stone says one of the reasons that he moved out of private practice and into academia was because of burn out associated with single-handedly dealing with the managed care issues in a solo practice, he says he thinks it’s ridiculous when he hears physicians say they are going to throw in the towel because of the evolution of healthcare. “We all learned to deal with CPT and everyone will learn to deal with ICD-10 and meaningful use and EMR [electronic medical record] and anything else that comes along. Things change. That’s life. If they are frustrated enough by these developments to consider retirement, they are probably ready anyway,” he says.

Retired dermatologist Steve Shama, MD, successfully parlayed a presentation on risk management that he frequently gave during his earlier medical career into a career as a motivational speaker. He says when the profession you once loved becomes more of a chore than a challenge, it’s time to consider a change. “Once you no longer love what you do because of negative pressures from government, hospitals or insurance companies then it may be time to say good-bye. Once I realized I didn’t love my job anymore, it was a very easy decision to move on.”

University of Massachusetts dermatologist Mary Maloney, MD, is just a few years away from what would conventionally be considered retirement age. “I think it’s really important to have a plan and to build your plan. If you haven’t built a plan, don’t retire. If you haven’t built a plan, start building one. Some of the most unhappy people I know are physicians who retired too soon. They think they want to kick back, but that gets boring really quickly.”

Her advice: “Try a trial retirement. Take a month off. How do you feel at the end of that month? If you’re bored, go back to work and begin to develop a plan for what work or volunteer activities you’ll take part in when you really retire. You became a physician because you have a type-A personality. You can’t just walk away from that,” she says.

When it comes to retirement or transitioning out of dermatology practice and into some other professional endeavor, practice management pundits and those who have been through the experience agree that: Those who fail to plan, plan to fail.

When it comes to retirement or transitioning out of dermatology practice and into some other professional endeavor, practice management pundits and those who have been through the experience agree that: Those who fail to plan, plan to fail.

It’s never too soon to start planning for retirement because there are so many boxes on the to-do list that need to be checked before a dermatologist can transition into the next phase of his or her life without leaving loose ends dangling (See Checklist).

[Read Part 2 of this series, Three Key Steps in Retirement Planning: Part 2 here].

Former American Academy of Dermatology President Stephen Stone, MD, Southern Illinois University (SIU), School of Medicine, Springfield, IL, says it’s always a good idea to engage an accountant and attorney who are familiar with medical practice issues so they can guide you along in the process that includes everything from wrapping up the employee pension plan to obtaining a “tail” that provides coverage against claims reported after your regular liability insurance policy expires. Dr. Stone started out as a partner in a dermatology practice. After 2 associates moved on to teaching positions, Dr. Stone decided that, he, too, would make a similar switch.

“The main reason I left private practice was that I was in a solo situation, and I was burning out with respect to the practice management and the business aspects of the practice. I still loved seeing patients and I loved working with residents, but I knew I had to make a change,” he explains. While he was in private practice, he was a volunteer faculty member at SIU, and he says the best part of that was working with the residents. “So when I had the opportunity to close up my practice and take a teaching position, it was a perfect fit,” says Dr. Stone.

One of the most difficult parts of closing his practice was sharing the news with his employees. “Frankly, that played a part in delaying my decision because most of them were with me for quite a while. We were like a family. Some of them moved on to the medical school with me, and others I tried to help find jobs,” he says.

On a more practical note, Dr. Stone stresses, “You can’t just shut the practice and walk away. It’s a pretty complicated process. You have to bear in mind that your bills are not going to go out until after the very last day you see patients and money is going to trickle in for over a year. So, you’ve got to have arrangements for receiving, depositing and continuing to bill the outstanding receivables, among other things.”

Live and Learn

Former private practice dermatologist Haines Ely, MD, of Grass Valley, CA, is the perfect example of a dermatologist who lacked key knowledge necessary to effectively close up shop. “Something that is not common knowledge is that your expenses don’t stop just because you close the doors of the office. You continue to receive requests for medical records, insurance forms, overpayment/underpayment billings from Medicare, insurance companies and others. The paperwork continues for months,” he says. “I assumed that when I closed the doors, everything stopped — but it didn’t. So I learned that you need a staff — or someone — to take care of the continuing trail of papers.” He says he still gets requests from insurance companies about claims submitted 2 to 3 years ago.

Valuing Your Practice

Bellville, NJ-based dermatologist and dermatology practice management guru Joseph Eastern, MD, frequently writes about and makes presentation on the topic of retirement. The 2-time past-president of the Dermatological Society of New Jersey says when considering what steps to take if or when you decide to sell your practice the first hurdle is the accurate valuation of the practice. “It’s important that the appraisal be done by an experienced and neutral financial consultant, that all techniques used in the valuation be divulged and explained and that documentation is supplied to support the conclusions reached,” says Dr. Eastern.

It’s important to recognize that the valuation will not necessarily equal the purchase price, other factors may need to be considered before a final price can be agreed upon and there may be legal constraints on the purchase price. “For example,” says Dr. Eastern, “if the buyer is a non-profit corporation such as a hospital or health maintenance organization (HMO), by law it cannot pay in excess of fair market value for the practice.”

Once a value has been agreed upon, the seller must consider how the transaction will be structured. “The most popular structures include purchase of assets, purchase of corporate stock or merger,” says Dr. Eastern. “Buyers, especially institutional buyers, prefer to purchase assets, because it allows them to pick and choose only those items that have value to them,” he explains. Depending on the circumstances, an asset sale may still be to both parties’ advantage. “Sellers typically prefer to sell stock because it allows them to sell their entire practice, which is often worth more than the sum of its parts, and often provides tax advantages,” adds Dr. Eastern.

The third option — merger — continues to grow in popularity. Usually, this takes the form of a sale of the medical practice to a publicly-traded HMO, which issues its own stock in payment, explains Dr. Eastern. “Because such purchasers are exempt from the restrictions that apply to not-for-profit organizations, they can pay higher prices — and pay for goodwill — and the stock issued in payment offers the seller an opportunity to participate in future profits and appreciation of value.”

Stock ownership is not without risk, of course, so he stresses that tax issues must always be considered. “Most private practices are corporations, and the sale of corporate stock will result in a long-term capital gain which will be taxed (under current law) at 28%. It actually may benefit the seller to accept a slightly lower price if the sale can be structured to provide significantly lower tax treatment. However, any gain that does not qualify as a long-term capital gain will be taxed as regular income — currently around 40%, plus a social security tax of about 15%,” explains Dr. Eastern.

The seller may wish to continue working at the practice as an employee, and this is often to the buyer’s advantage as well, points out Dr. Eastern. “Transitioning to new ownership in stages often maximizes the value of the business by improving patient retention, and allows patients to become accustomed to the transition. However, care must be taken, with the aid of good legal advice, to structure such an arrangement in a way that minimizes concerns of fraud and abuse. Congress has created a “safe harbor” to allow continuing employment, but its scope is narrow and does not cover many common arrangements. To qualify, the sale of the practice, including any installment payments, must be completed within a year after an agreement is reached, and the seller cannot be in a position to make referrals to the buyer after a year.”

Just (Don’t) Do It

Las Vegas dermatologist Lucius Blanchard, MD, knows more about selling — and buying — dermatology practices than the average physician. His large group practice, Las Vegas Skin and Cancer Clinics acquired practices throughout Arizona and California a few years back when market conditions were better. “The problem with trying to sell a dermatology practice,” says Dr. Blanchard, “is that I can go somewhere and open a dermatology office for approximately $100,000 — depending on the area — and I can equip it, and put a physician in there, and in a year or two build up a very good practice. So why would I pay somebody $400,000 or $500,000 for a practice unless they are going to stay there for a few years to generate income and ensure that the patient base keeps growing. If they just want to sell and leave, there’s little value there.” Dr. Blanchard started off with 2 other dermatologists in 1 office and now has 25 offices throughout California, Arizona and Nevada.

Dr. Blanchard’s retirement advice to fellow dermatologists: Don’t do it. “As long as you’re healthy and can work, don’t retire. We have one of the best jobs anyone could have. It’s office-based, there’s very little emergency work and we don’t have as much risk as other specialists such as cardiovascular surgeons,” says Dr. Blanchard, “Plus, we can even selectively limit ourselves to low risk patients if we want to and limit our office hours so that we can structure our life pretty much how we want it to be.”

Despite Dr. Blanchard’s anti-retirement recommendation, clearly every dermatologist eventually reaches the point when passing the baton is appealing — or necessary. Some move on because they reach an age that they decided years before would be the appropriate time to make a change; others because their retirement account reaches a value that they decided years before would be adequate to support them through their twilight years and still others because they have had enough of managed care, government intervention, insurance company interference, complex electronic medical record technology and the mandate to document its meaningful use in order to avoid fines.

Dr. Ely says he would prefer to still be in private practice, but because of governmental interference he literally cannot afford to. It’s what prompted his retirement and his switch to academia. He is now a professor at University of California, Davis. “In 2011 my office manager informed me that by 2013, the graph of income versus expenses would cross in our practice and I would be working for nothing. By February of 2013, the lines crossed, and she came to me and said, ‘You are now officially working for nothing. Your expenses and your income are the same.’ I had no choice but to move on,” says Dr. Ely.

He explains, “I practiced in a small community with an independent practice association (IPA) that did the billing for all the physicians in the practice. Medicare audited the IPA and we were told that [Medicare] had to withhold a large amount of money for future claims, so the IPA had to withhold money from all of our claims, which diminished our income dramatically and the expenses kept going up.” He says he misses his private practice patients and the dynamic inherent in developing long-term connections with them. “I’m still seeing patients with residents, and that’s enjoyable, but it would have been nice to be able to stay in private practice,” he says.

While Dr. Stone says one of the reasons that he moved out of private practice and into academia was because of burn out associated with single-handedly dealing with the managed care issues in a solo practice, he says he thinks it’s ridiculous when he hears physicians say they are going to throw in the towel because of the evolution of healthcare. “We all learned to deal with CPT and everyone will learn to deal with ICD-10 and meaningful use and EMR [electronic medical record] and anything else that comes along. Things change. That’s life. If they are frustrated enough by these developments to consider retirement, they are probably ready anyway,” he says.

Retired dermatologist Steve Shama, MD, successfully parlayed a presentation on risk management that he frequently gave during his earlier medical career into a career as a motivational speaker. He says when the profession you once loved becomes more of a chore than a challenge, it’s time to consider a change. “Once you no longer love what you do because of negative pressures from government, hospitals or insurance companies then it may be time to say good-bye. Once I realized I didn’t love my job anymore, it was a very easy decision to move on.”

University of Massachusetts dermatologist Mary Maloney, MD, is just a few years away from what would conventionally be considered retirement age. “I think it’s really important to have a plan and to build your plan. If you haven’t built a plan, don’t retire. If you haven’t built a plan, start building one. Some of the most unhappy people I know are physicians who retired too soon. They think they want to kick back, but that gets boring really quickly.”

Her advice: “Try a trial retirement. Take a month off. How do you feel at the end of that month? If you’re bored, go back to work and begin to develop a plan for what work or volunteer activities you’ll take part in when you really retire. You became a physician because you have a type-A personality. You can’t just walk away from that,” she says.

When it comes to retirement or transitioning out of dermatology practice and into some other professional endeavor, practice management pundits and those who have been through the experience agree that: Those who fail to plan, plan to fail.

It’s never too soon to start planning for retirement because there are so many boxes on the to-do list that need to be checked before a dermatologist can transition into the next phase of his or her life without leaving loose ends dangling (See Checklist).

[Read Part 2 of this series, Three Key Steps in Retirement Planning: Part 2 here].

Former American Academy of Dermatology President Stephen Stone, MD, Southern Illinois University (SIU), School of Medicine, Springfield, IL, says it’s always a good idea to engage an accountant and attorney who are familiar with medical practice issues so they can guide you along in the process that includes everything from wrapping up the employee pension plan to obtaining a “tail” that provides coverage against claims reported after your regular liability insurance policy expires. Dr. Stone started out as a partner in a dermatology practice. After 2 associates moved on to teaching positions, Dr. Stone decided that, he, too, would make a similar switch.

“The main reason I left private practice was that I was in a solo situation, and I was burning out with respect to the practice management and the business aspects of the practice. I still loved seeing patients and I loved working with residents, but I knew I had to make a change,” he explains. While he was in private practice, he was a volunteer faculty member at SIU, and he says the best part of that was working with the residents. “So when I had the opportunity to close up my practice and take a teaching position, it was a perfect fit,” says Dr. Stone.

One of the most difficult parts of closing his practice was sharing the news with his employees. “Frankly, that played a part in delaying my decision because most of them were with me for quite a while. We were like a family. Some of them moved on to the medical school with me, and others I tried to help find jobs,” he says.

On a more practical note, Dr. Stone stresses, “You can’t just shut the practice and walk away. It’s a pretty complicated process. You have to bear in mind that your bills are not going to go out until after the very last day you see patients and money is going to trickle in for over a year. So, you’ve got to have arrangements for receiving, depositing and continuing to bill the outstanding receivables, among other things.”

Live and Learn

Former private practice dermatologist Haines Ely, MD, of Grass Valley, CA, is the perfect example of a dermatologist who lacked key knowledge necessary to effectively close up shop. “Something that is not common knowledge is that your expenses don’t stop just because you close the doors of the office. You continue to receive requests for medical records, insurance forms, overpayment/underpayment billings from Medicare, insurance companies and others. The paperwork continues for months,” he says. “I assumed that when I closed the doors, everything stopped — but it didn’t. So I learned that you need a staff — or someone — to take care of the continuing trail of papers.” He says he still gets requests from insurance companies about claims submitted 2 to 3 years ago.

Valuing Your Practice

Bellville, NJ-based dermatologist and dermatology practice management guru Joseph Eastern, MD, frequently writes about and makes presentation on the topic of retirement. The 2-time past-president of the Dermatological Society of New Jersey says when considering what steps to take if or when you decide to sell your practice the first hurdle is the accurate valuation of the practice. “It’s important that the appraisal be done by an experienced and neutral financial consultant, that all techniques used in the valuation be divulged and explained and that documentation is supplied to support the conclusions reached,” says Dr. Eastern.

It’s important to recognize that the valuation will not necessarily equal the purchase price, other factors may need to be considered before a final price can be agreed upon and there may be legal constraints on the purchase price. “For example,” says Dr. Eastern, “if the buyer is a non-profit corporation such as a hospital or health maintenance organization (HMO), by law it cannot pay in excess of fair market value for the practice.”

Once a value has been agreed upon, the seller must consider how the transaction will be structured. “The most popular structures include purchase of assets, purchase of corporate stock or merger,” says Dr. Eastern. “Buyers, especially institutional buyers, prefer to purchase assets, because it allows them to pick and choose only those items that have value to them,” he explains. Depending on the circumstances, an asset sale may still be to both parties’ advantage. “Sellers typically prefer to sell stock because it allows them to sell their entire practice, which is often worth more than the sum of its parts, and often provides tax advantages,” adds Dr. Eastern.

The third option — merger — continues to grow in popularity. Usually, this takes the form of a sale of the medical practice to a publicly-traded HMO, which issues its own stock in payment, explains Dr. Eastern. “Because such purchasers are exempt from the restrictions that apply to not-for-profit organizations, they can pay higher prices — and pay for goodwill — and the stock issued in payment offers the seller an opportunity to participate in future profits and appreciation of value.”

Stock ownership is not without risk, of course, so he stresses that tax issues must always be considered. “Most private practices are corporations, and the sale of corporate stock will result in a long-term capital gain which will be taxed (under current law) at 28%. It actually may benefit the seller to accept a slightly lower price if the sale can be structured to provide significantly lower tax treatment. However, any gain that does not qualify as a long-term capital gain will be taxed as regular income — currently around 40%, plus a social security tax of about 15%,” explains Dr. Eastern.

The seller may wish to continue working at the practice as an employee, and this is often to the buyer’s advantage as well, points out Dr. Eastern. “Transitioning to new ownership in stages often maximizes the value of the business by improving patient retention, and allows patients to become accustomed to the transition. However, care must be taken, with the aid of good legal advice, to structure such an arrangement in a way that minimizes concerns of fraud and abuse. Congress has created a “safe harbor” to allow continuing employment, but its scope is narrow and does not cover many common arrangements. To qualify, the sale of the practice, including any installment payments, must be completed within a year after an agreement is reached, and the seller cannot be in a position to make referrals to the buyer after a year.”

Just (Don’t) Do It

Las Vegas dermatologist Lucius Blanchard, MD, knows more about selling — and buying — dermatology practices than the average physician. His large group practice, Las Vegas Skin and Cancer Clinics acquired practices throughout Arizona and California a few years back when market conditions were better. “The problem with trying to sell a dermatology practice,” says Dr. Blanchard, “is that I can go somewhere and open a dermatology office for approximately $100,000 — depending on the area — and I can equip it, and put a physician in there, and in a year or two build up a very good practice. So why would I pay somebody $400,000 or $500,000 for a practice unless they are going to stay there for a few years to generate income and ensure that the patient base keeps growing. If they just want to sell and leave, there’s little value there.” Dr. Blanchard started off with 2 other dermatologists in 1 office and now has 25 offices throughout California, Arizona and Nevada.

Dr. Blanchard’s retirement advice to fellow dermatologists: Don’t do it. “As long as you’re healthy and can work, don’t retire. We have one of the best jobs anyone could have. It’s office-based, there’s very little emergency work and we don’t have as much risk as other specialists such as cardiovascular surgeons,” says Dr. Blanchard, “Plus, we can even selectively limit ourselves to low risk patients if we want to and limit our office hours so that we can structure our life pretty much how we want it to be.”

Despite Dr. Blanchard’s anti-retirement recommendation, clearly every dermatologist eventually reaches the point when passing the baton is appealing — or necessary. Some move on because they reach an age that they decided years before would be the appropriate time to make a change; others because their retirement account reaches a value that they decided years before would be adequate to support them through their twilight years and still others because they have had enough of managed care, government intervention, insurance company interference, complex electronic medical record technology and the mandate to document its meaningful use in order to avoid fines.

Dr. Ely says he would prefer to still be in private practice, but because of governmental interference he literally cannot afford to. It’s what prompted his retirement and his switch to academia. He is now a professor at University of California, Davis. “In 2011 my office manager informed me that by 2013, the graph of income versus expenses would cross in our practice and I would be working for nothing. By February of 2013, the lines crossed, and she came to me and said, ‘You are now officially working for nothing. Your expenses and your income are the same.’ I had no choice but to move on,” says Dr. Ely.

He explains, “I practiced in a small community with an independent practice association (IPA) that did the billing for all the physicians in the practice. Medicare audited the IPA and we were told that [Medicare] had to withhold a large amount of money for future claims, so the IPA had to withhold money from all of our claims, which diminished our income dramatically and the expenses kept going up.” He says he misses his private practice patients and the dynamic inherent in developing long-term connections with them. “I’m still seeing patients with residents, and that’s enjoyable, but it would have been nice to be able to stay in private practice,” he says.

While Dr. Stone says one of the reasons that he moved out of private practice and into academia was because of burn out associated with single-handedly dealing with the managed care issues in a solo practice, he says he thinks it’s ridiculous when he hears physicians say they are going to throw in the towel because of the evolution of healthcare. “We all learned to deal with CPT and everyone will learn to deal with ICD-10 and meaningful use and EMR [electronic medical record] and anything else that comes along. Things change. That’s life. If they are frustrated enough by these developments to consider retirement, they are probably ready anyway,” he says.

Retired dermatologist Steve Shama, MD, successfully parlayed a presentation on risk management that he frequently gave during his earlier medical career into a career as a motivational speaker. He says when the profession you once loved becomes more of a chore than a challenge, it’s time to consider a change. “Once you no longer love what you do because of negative pressures from government, hospitals or insurance companies then it may be time to say good-bye. Once I realized I didn’t love my job anymore, it was a very easy decision to move on.”

University of Massachusetts dermatologist Mary Maloney, MD, is just a few years away from what would conventionally be considered retirement age. “I think it’s really important to have a plan and to build your plan. If you haven’t built a plan, don’t retire. If you haven’t built a plan, start building one. Some of the most unhappy people I know are physicians who retired too soon. They think they want to kick back, but that gets boring really quickly.”

Her advice: “Try a trial retirement. Take a month off. How do you feel at the end of that month? If you’re bored, go back to work and begin to develop a plan for what work or volunteer activities you’ll take part in when you really retire. You became a physician because you have a type-A personality. You can’t just walk away from that,” she says.